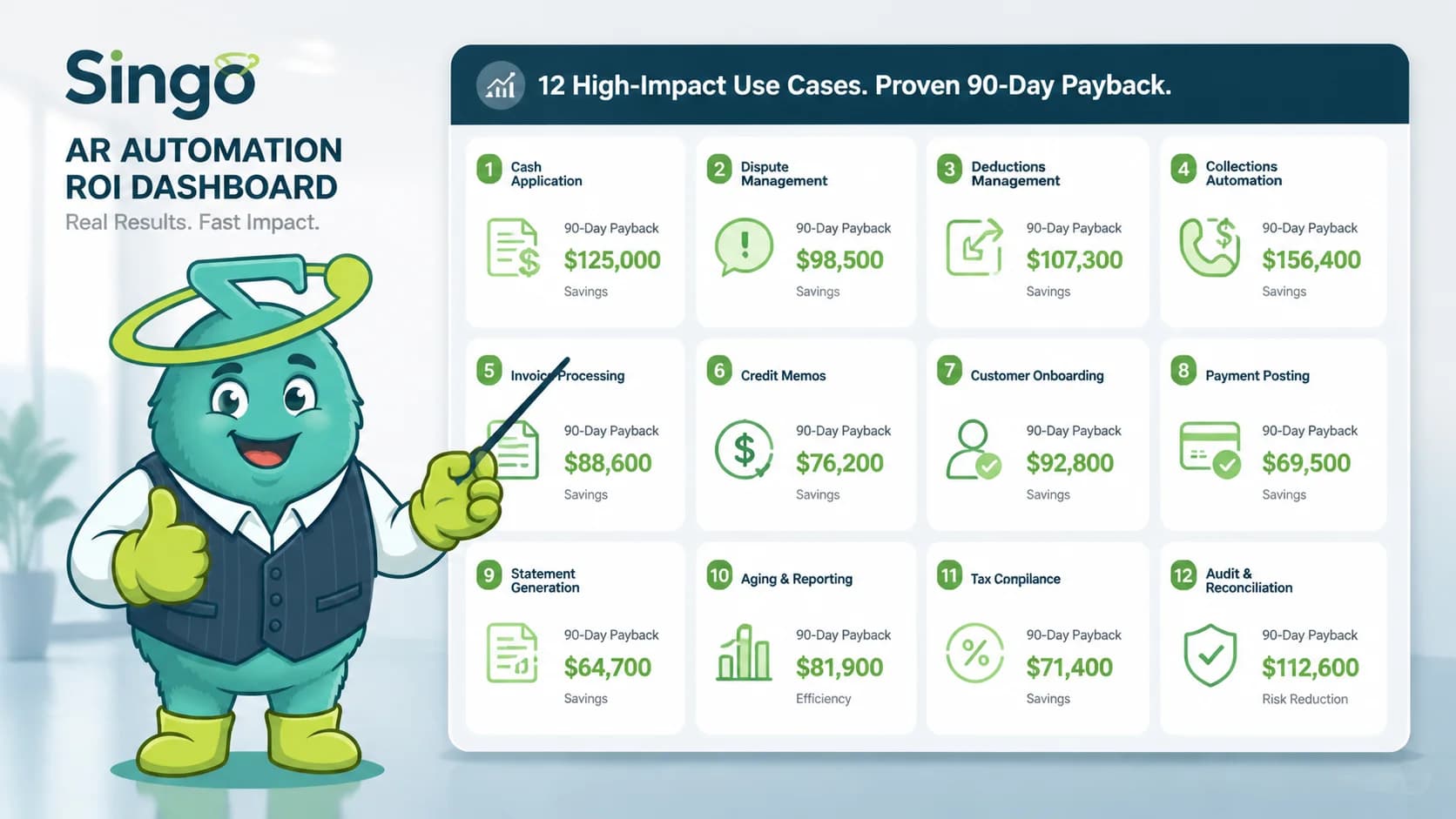

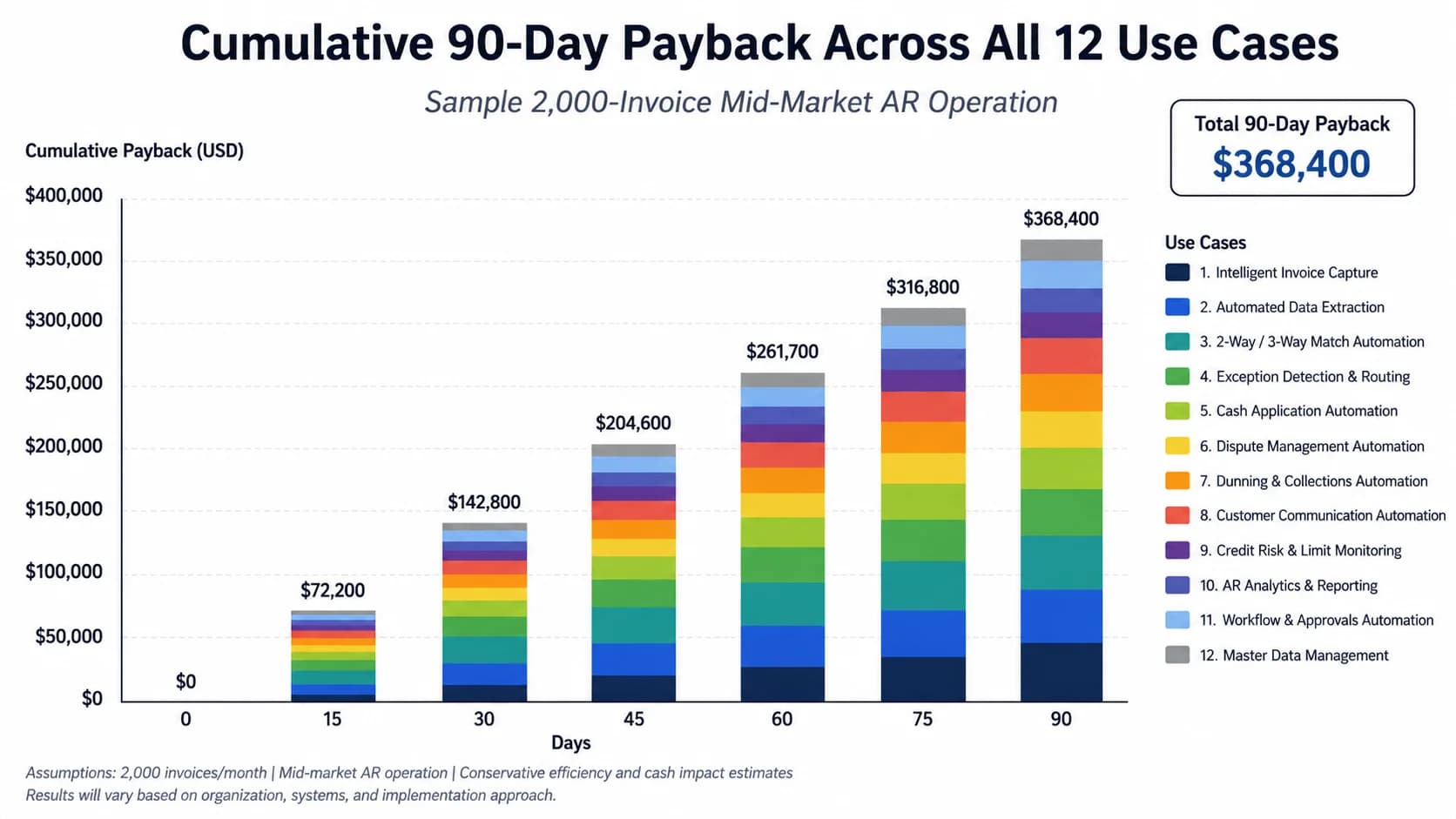

Quick Summary

The 12 highest-ROI AR automation use cases include cash application, dunning sequences, credit risk scoring, deduction management, dispute workflow, e-invoice delivery, payment portal, predictive pay-date, AR reporting, lockbox parsing, credit onboarding, and ERP cash posting.

Key Takeaways

- Cash application is the fastest-paying use case, with 90-95% straight-through match rates saving 60-80 hours per month and typically paying back in 30-45 days.

- Stacked DSO reduction across dunning, invoice delivery, portal, and predictive pay-date totals 15-25 days; each day equals roughly $2,740 of working capital per $1M revenue.

- Credit risk scoring and deduction recovery deliver the largest direct EBITDA lift, cutting bad-debt 30-40% and recovering 30-50% of disputed deductions.

- Not every use case pays back in 90 days; ERP cash posting and credit onboarding usually take 120-180 days but compound ROI in years two and three.

- A 2,000-invoice mid-market AR operation typically returns 3-5x the annual software cost within 90 days, even on conservative input assumptions.

Calculate your AR automation ROI

Plug in your monthly invoice volume, average DSO, and bad-debt rate to see your 90-day cumulative payback across all 12 use cases.

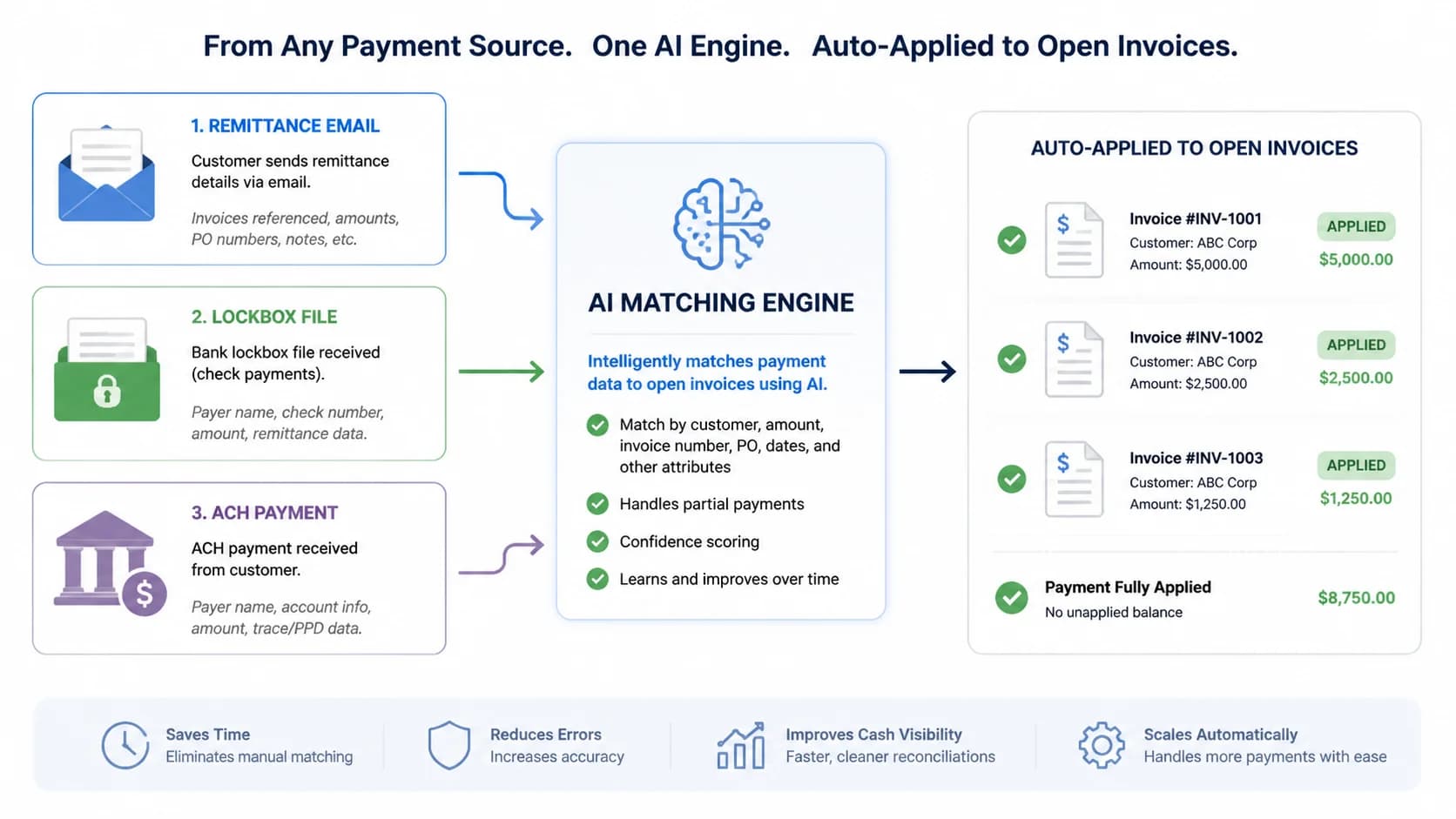

AI cash application and payment matching

AI cash application matches incoming payments to open invoices automatically, typically achieving 90-95% straight-through processing and saving 60-80 hours per month for a 2,000-invoice operation, with payback inside 30-45 days at typical manual cost-per-invoice rates.

Cash application is the highest-volume, lowest-judgment task on the AR desk, which is exactly why it is the first place to automate. An AI matching engine ingests remittance from emails, PDFs, lockbox files, and ACH/wire metadata, then matches dollars to open invoices with confidence scoring. Top-tier engines hit 90-95% straight-through match rates within the first 60 days. The 5-10% that requires human review gets routed with full context attached, so analysts spend minutes per exception instead of digging through inboxes.

The payback math here is the cleanest in the entire AR stack. A 2,000-invoice operation typically logs 60-80 hours per month on manual application work. At a fully-loaded analyst rate of $40 per hour, that is $2,400-$3,200 in monthly labor savings before you count error reduction, faster month-end close, or the hidden cost of misapplied cash. Read more about the scale of this problem in [the $47B manual AR processing problem](/blog/47-billion-ar-problem-manual-invoice-processing) for context on industry-wide labor drain.

Per AFP cash application benchmarks, the average company applies cash with 65-70% straight-through rates manually, so AI lifts the rate by roughly 25 percentage points. That delta is where 30-45 day payback comes from. Start here and you build internal trust for every use case below.

Pro Tip

Cash application is almost always the highest-ROI first automation. Start here even if you are nervous about scope, because it pays back fastest and creates internal credibility for the next eleven use cases.

Automated collections dunning sequences

Automated dunning sequences send pre-due, due-date, and escalation reminders across email, SMS, and customer portal, typically reducing DSO by 8-15 days within 60 days and freeing AR collectors to focus on the 20% of accounts that drive 80% of overdue balances.

Manual collections starts with a spreadsheet of aged invoices and ends with whoever has time sending the same template email. That model breaks the moment your AR team grows past 500 active customers. Automated dunning replaces it with a rules-based cadence: pre-due nudge at day -7, friendly reminder at day +3, firmer follow-up at day +14, escalation at day +30, each sent across the channel the customer responds to fastest. Customers who ignore email often respond to SMS within an hour.

The DSO impact is the headline number. Most mid-market AR teams see DSO drop 8-15 days inside 60 days of switching on multi-channel dunning. Apply that to a $50M revenue business and you are looking at $1.1M-$2.0M in released working capital, available to fund payroll, inventory, or debt paydown without a credit line draw. For a deeper look at the systems behind this, see [proven DSO reduction strategies](/blog/reduce-dso-proven-strategies-2026) which break down each lever individually.

Payback typically lands in 45-75 days. The catch: cadences need tuning. Sending too aggressively damages customer relationships; too softly and DSO barely moves. Plan for a 30-day calibration window.

Pro Tip

Add a pre-due reminder 5-7 days before the due date. This single addition typically captures 15-20% of late payments before they ever cross into delinquent status.

AI credit risk scoring and monitoring

AI credit risk scoring continuously reviews customer financial signals, payment history, and external data to flag deteriorating accounts before they default, typically cutting bad-debt write-offs by 30-40% and dropping the savings straight to operating income.

Most AR teams review customer credit annually if at all. By the time anyone notices the deterioration, the customer is already 90 days past due and the receivable is heading to write-off. AI credit scoring fixes the cadence problem by monitoring customers continuously: bureau pulls, payment-behavior trends, public filings, even news signals. When a score drops, the system flags the account for credit-hold review or proactive outreach before the next order ships.

The financial impact is direct. A mid-market business carrying $50M in revenue with a 0.8% bad-debt rate writes off $400K per year. A 35% reduction is $140K dropping straight to EBITDA, with no offsetting cost increase. Per Forrester 2026 AR automation trend research, top-quartile teams using AI credit monitoring run bad-debt rates 40-50% below their industry medians.

Payback for credit scoring is harder to predict than cash application because losses are lumpy. One avoided large default can pay for the entire AR automation stack for two years. The conservative way to model it: use your trailing 24-month average write-off rate, apply a 30% reduction, and treat that as floor savings. Anything above is upside.

See SINGOA in action

Mid-market AR teams using SINGOA collect 35% faster on the same headcount and recover bad-debt write-offs other tools miss. See it live.

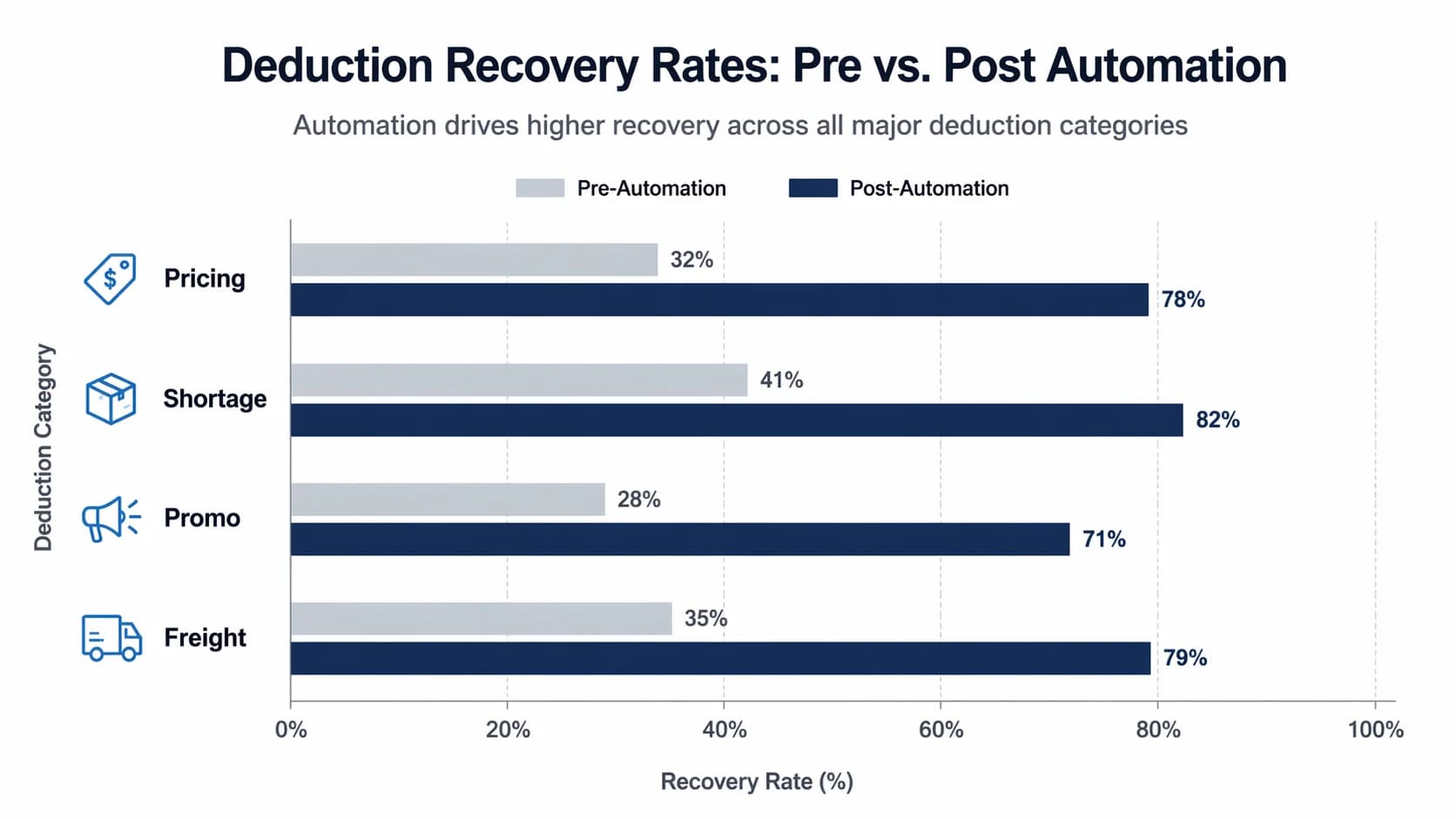

Deduction and short-pay management

Deduction management automation classifies short-pays by reason code, routes each to the correct internal owner, and enforces resolution SLAs, typically recovering 30-50% of unauthorized deductions previously written off as too costly to chase.

Short-pays and deductions are the silent margin leak in wholesale, manufacturing, and CPG. A customer pays $9,400 against a $10,000 invoice, attaches a one-line note about a freight charge, and the AR team writes off the $600 because investigating costs more than the recovery. Multiply that across hundreds of monthly deductions and you have a five-to-six-figure annual leak the income statement never explicitly shows.

Automated deduction management classifies each short-pay by reason code (pricing, shortage, promotional allowance, freight, return), routes it to the team that owns the resolution (Sales for pricing, Logistics for shortage, Marketing for promo), and enforces an SLA clock. Recovery rates of 30-50% on previously-written-off deductions are realistic in the first 90 days. For a business carrying $200K in annual deduction write-offs, that is $60K-$100K returned directly to gross margin.

The structural win goes beyond dollars. A reason-coded deduction database becomes the most honest customer-behavior dataset your finance team owns. Patterns emerge fast: which customers stack promotional deductions, which sales reps over-promise terms. That intelligence is worth as much as the recovered cash, especially during contract renewal negotiations.

Pro Tip

Track recovery rate by deduction reason code. Pricing and promotional deductions usually carry the highest recovery yield, so prioritize those queues for human review and route lower-yield codes to bulk auto-resolution rules.

Dispute resolution workflow automation

Automated dispute workflows route customer disputes to the correct internal owner with full transaction context, enforce resolution SLAs, and typically cut average dispute resolution time from 30+ days to 8-12 days while releasing AR trapped in dispute status.

Disputes live in email threads. A customer flags a billing question, AR forwards it to the account manager, the account manager loops in operations, three weeks pass, and the invoice sits in dispute the entire time. That trapped AR does not show up on the aging report because everyone considers it 'in process,' but it is real working capital sitting still.

Automated dispute workflows put structure on the chaos. Each dispute gets a ticket with the invoice, supporting documents, customer correspondence, and an assigned owner with an SLA clock. Escalation rules ping the next level if the SLA breaches. Average resolution time drops 60% (from 30+ days to 8-12) once the system enforces accountability, and the AR aging report finally tells the truth about what is actually disputed versus what is simply delayed.

The hidden upside: disputes resolved faster also recover full payment more often. Customers expect rapid response, and a 9-day resolution is far less likely to escalate into a credit memo than a 35-day one. Plan to see resolution time improve before you see write-off reduction.

Electronic invoice delivery and tracking

Electronic invoice delivery confirms invoice receipt with timestamps, read events, and bounce detection, eliminating the 'I never got it' excuse and accelerating customer payment by 5-7 days while removing the labor burden of manual re-sends.

The most common collections excuse is also the hardest to disprove without infrastructure: 'we never received the invoice.' If your team mails PDFs from a shared inbox, that statement is technically unverifiable. The customer holds the timeline, your AR team holds nothing. Electronic delivery flips that asymmetry by attaching delivery confirmation, read receipts, click events, and bounce alerts to every send.

DSO impact runs 5-7 days for businesses migrating off PDF-by-email. The math is simple: roughly 8-12% of invoices in manual workflows trigger a re-send cycle that adds two weeks to payment. Killing that cycle compresses average days-to-pay across the entire AR book. For a $25M business, even a 5-day DSO improvement releases $342,000 in working capital using the standard $2,740-per-day-per-million benchmark.

Bounce detection is the underrated feature. When AR can see that an invoice landed in a spam folder or hit an old AP contact, the team intervenes the same day instead of three weeks later. That single signal prevents the slow-walk into a 60-day bucket more often than any dunning template ever will.

Pro Tip

Pair invoice delivery with a 'Pay Now' button embedded directly in the email. Embedded payment links convert 40-60% better than portal-only flows because they remove the login friction step entirely.

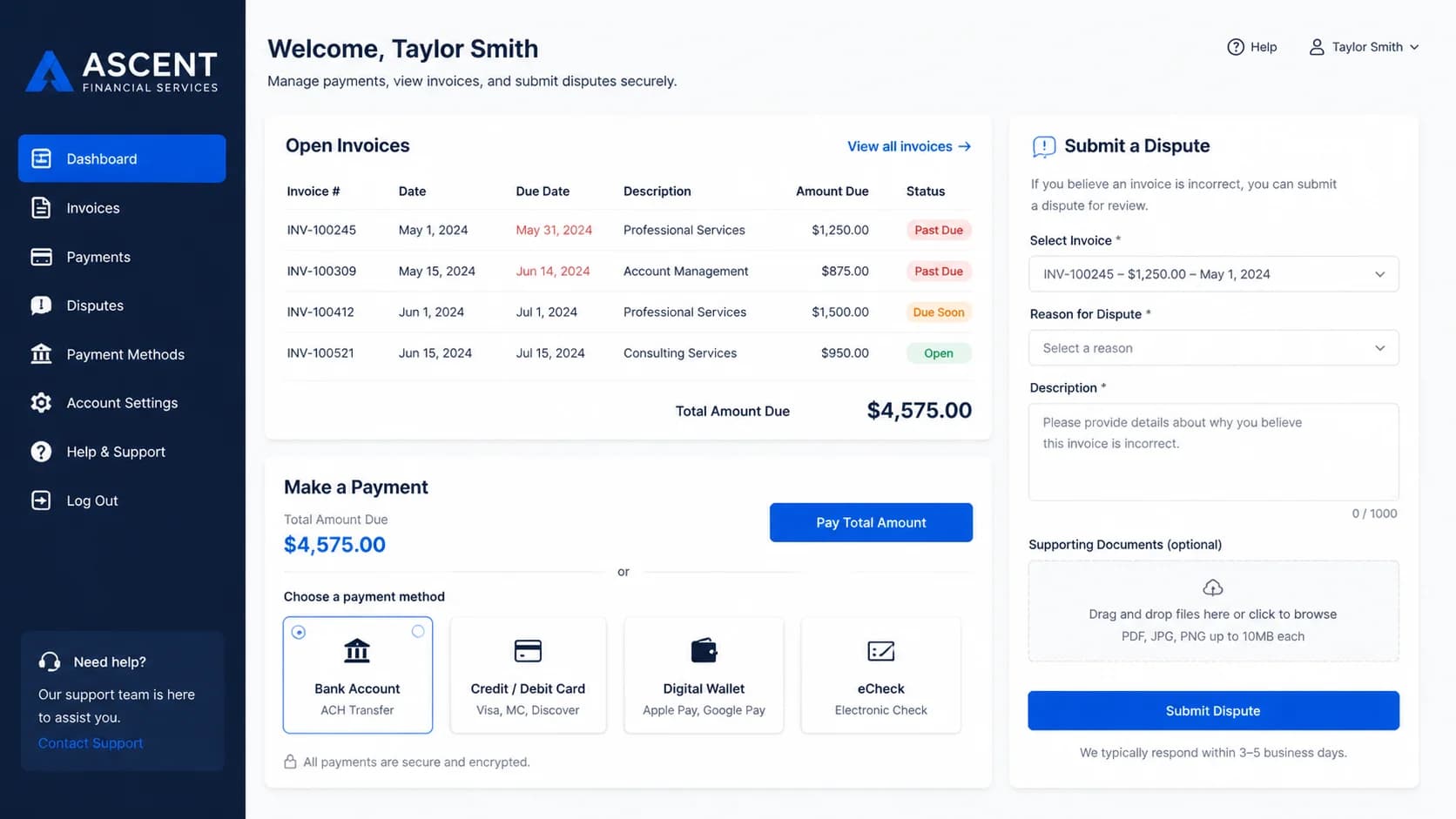

Branded customer payment portal (self-service)

A branded customer payment portal lets customers view open invoices, download statements, dispute charges, and pay via ACH or card on their own schedule, typically deflecting 40-60% of inbound AR inquiries that would otherwise hit the team's shared inbox.

Inbound 'where is my invoice' and 'can you resend the statement' emails consume a surprising share of an AR analyst's day. Industry benchmarks put inquiry volume at 1.2 to 1.8 messages per active customer per month. For a 500-customer book, that is roughly 600-900 inquiries arriving every month, each one taking 4-8 minutes to handle. Self-service deflects 40-60% of that load on day one.

The portal also moves payment timing earlier. Customers who can pay any time, from any device, with autopay options for recurring invoices, almost always settle faster than customers chasing a paper check approval. ACH and card-on-file payments inside [SINGOA's payment portal](/features) typically lift the share of invoices paid before the due date from 35% to over 60% within the first quarter.

Hours redirected from inquiry triage move to high-value collection work, the 90-plus aging bucket where one human conversation recovers more cash than fifty automated reminders. That reallocation is the real ROI lever, not the portal feature list.

Predictive payment date forecasting

Machine learning predicts when each individual invoice will actually be paid based on customer payment history, invoice size, and seasonality patterns, improving 13-week cash forecast accuracy by 25-35% over flat 'due-date plus average DSO' assumptions.

Treasury teams build 13-week cash forecasts off AR aging plus a flat assumption: customers pay 12 days late on average, so push every invoice forward 12 days. That works for the aggregate but fails badly per customer. Some accounts are predictably 30 days slow, others pay early, and the average smears both signals into noise. Predictive models score each invoice individually and produce a probability-weighted pay date.

The accuracy lift is meaningful: 25-35% reduction in forecast variance against actuals. Treasury translates that into deployable working capital. When the CFO can trust that $1.4M is landing in week six rather than 'somewhere in weeks five through eight,' idle balances get put into short-term instruments or used to draw down revolvers earlier.

The same predictions feed collections prioritization. If the model says a particular invoice will pay 18 days late even with reminders, the collector can intervene three weeks earlier instead of waiting for it to age. See [AR KPIs every CFO should track](/blog/accounts-receivable-kpis-cfo-track) for how to integrate predicted DSO into board reporting.

AR aging and DSO reporting automation

Automated AR reporting eliminates the monthly spreadsheet build by refreshing DSO, CEI, aging buckets, and bad-debt ratio from live ERP data daily, saving an average of 15-25 analyst hours every month while giving leadership weekly trend visibility instead of monthly snapshots.

The monthly AR report is the most-built spreadsheet in finance. An analyst pulls the aging from the ERP, builds bucket totals in Excel, calculates DSO and CEI from raw transaction data, and rebuilds the same charts the prior month already had. IOFM's cost-per-invoice benchmark work consistently shows this manual reporting cycle eats 15-25 hours a month at most mid-market companies, and the output is already stale by the time it lands on the CFO's desk.

Automated reporting refreshes the same metrics from live ERP data, usually daily. The shift from monthly to weekly cadence catches deterioration 3-4 weeks earlier than monthly review can. A 4-day DSO uptick spotted in week one of the month is recoverable. The same uptick spotted six weeks later is already trapped in a 60-plus aging bucket where collection probability drops sharply.

Boards also start asking different questions when they see weekly trend lines instead of single monthly points. The conversation shifts from 'what happened last month' to 'what is happening right now,' which is the conversation that actually drives interventions.

Pro Tip

Switch from monthly to weekly DSO review. Weekly visibility catches deterioration 3-4 weeks earlier, when accounts are still in the under-30 bucket and a single phone call still recovers most of them.

Lockbox and bank file reconciliation

Automated lockbox parsing ingests BAI2, CAMT, and bank lockbox files, extracts remittance advice, matches to open invoices, and posts cash directly to the ERP, eliminating 8-12 hours per week of manual reconciliation at most mid-market AR operations.

Lockbox processing is one of those tasks that looks small until you measure it. Someone downloads the BAI2 file every morning, opens the remittance PDFs that arrived overnight, cross-references customer names against the ERP, and keys in payment applications one by one. For a 2,000-invoice operation, that workflow consumes 8-12 hours every week, and the analyst doing it is rarely the most junior person on the team.

Automation parses the same files in seconds. The system reads BAI2 and CAMT formats natively, extracts remittance advice from email attachments and lockbox images, and matches payments to open invoices using the same logic as core cash application. When confidence is high, cash posts straight to the ERP without human review.

The downstream effect shows up at month-end. Closes that used to slip a day or two waiting for unapplied cash to clear now run on schedule because the unapplied bucket never grew in the first place. Controllers consistently report this is the use case their team feels first, even though it rarely tops a vendor's marketing page.

Customer credit application and onboarding

Automated credit applications convert paper PDF intake into digital workflows with bureau pulls, trade reference checks, and rule-based approval routing, cutting new-customer onboarding from a typical 5-10 days down to under 24 hours for most low-risk applicants.

The credit application is usually where the Sales-vs-Finance friction starts. Sales closes a deal Friday afternoon, the customer needs to ship product Monday, and the credit application is a six-page PDF that needs to be printed, signed, scanned, emailed, and entered into the ERP by hand. Bureau pulls happen mid-week. Trade references are still phoned. The deal cools while everyone waits.

Digital intake collapses that timeline. The customer fills a web form, the system pulls a bureau report automatically, trade references go out as automated email surveys, and a rules engine approves or escalates based on configurable risk thresholds. Low-risk accounts approve in minutes. Higher-risk applications route to a human credit analyst with all signals already attached.

The revenue impact is direct and measurable: a sales cycle that used to lose 5-10 days waiting for credit approval shrinks to less than a day. For a business closing 30 new accounts a month at $15,000 average first-order value, that acceleration alone is worth several hundred thousand dollars in pulled-forward revenue every quarter.

Pro Tip

Tie the credit application directly to your CRM so Sales sees real-time approval status. This single integration removes the most common Sales-vs-Finance friction point, the 'where is my customer's credit decision' Slack message.

ERP-integrated cash posting and journal entries

Bidirectional ERP integration posts applied cash, adjustments, and write-offs back to the GL automatically with a built-in audit trail, eliminating duplicate data entry between the AR platform and systems like NetSuite, Sage Intacct, or QuickBooks, and shaving 1-2 days off month-end close.

AR automation that does not write back to the ERP is just a fancy collections inbox. The hours saved upstream get spent re-keying entries downstream, and the controller still cannot trust the GL balance until someone reconciles by hand. True ROI requires two-way sync that posts cash applications, deduction write-offs, dispute credits, and reclassifications back to the source of truth, with full audit trail attached to every transaction.

Connectors to NetSuite, Sage Intacct, QuickBooks, Microsoft Dynamics, and Acumatica are now table stakes. The right [ERP integrations](/integrations) handle multi-entity, multi-currency, and custom GL mappings without forcing the AR team to become integration engineers. When a payment posts in the AR platform, the journal entry hits the GL within minutes, not at the next overnight batch.

The compounding payoff lands at month-end. Closes that used to run 7-9 business days routinely drop to 5-6 once cash posting, deductions, and write-offs flow automatically. That recovered close time is what lets controllers move from reactive reporting to forward-looking analysis, the work that actually changes how the business is run.

ERP posting is one of the use cases that typically takes 120-180 days to fully pay back rather than 90, but it is the foundation that lets every other use case compound in years two and three.

Quick wins to roll out alongside the 12 use cases

Even before the full 12-use-case stack is live, these foundational habits compound the payback math and shorten the calibration window for every workflow above.